Introduction

“We see an acceleration because of AI workloads. More data is being used for training of models, more data is being used for inference and that by itself creates more data that needs to be stored.”

Kris Sennesael, WD CFO (February 2026)

As AI continues its rapid advancement, new bottlenecks are emerging across the ecosystem. Much of the investor focus has centred on compute, energy and memory, but storage has also emerged as a critical constraint. AI workloads both consume vast amounts of data and generate enormous new volumes that must be stored, moved and accessed efficiently. This demand is primarily met by two technologies: hard disk drives (HDDs), which offer the lowest cost per unit of storage, and NAND flash-based solid-state drives (SSDs), which offer higher performance. Together, they form complementary layers of the storage stack, with HDDs handling bulk capacity and SSDs serving higher-speed workloads.

“In the last 150 years ... 15 billion images were created. With AI, that same number of images was created only in the last one and a half years.”

B.S. Teh., Seagate COO (May 2025)

The sharp rise in demand has supported stronger revenues and profitability for storage manufacturers and driven significant share price appreciation. SanDisk, a NAND/SSD pure-play, has seen its shares rise roughly 20x over the past year, while HDD leaders Western Digital and Seagate are up approximately 9x and 7x, respectively. At the same time, the sector’s historic cyclicality remains an obvious concern, though management teams argue that AI is creating a more secular long-term demand backdrop rather than a traditional boom-and-bust cycle. This is reflected in customers placing greater emphasis on security of supply and increasingly signing multi-year agreements, which should provide greater price and demand stability going forwards. However, whether this marks a lasting shift in industry structure over the longer-term remains an open question.

In this note, we trace how AI-driven demand is reshaping the storage value chain, from the component manufacturers producing HDDs and NAND flash through to the enterprise platforms that package storage into solutions for end customers. We use SanDisk and Everpure (formerly Pure Storage) as case studies to illustrate how this demand is flowing through at each level.

Hard Disk Drives

HDDs are relatively slow in terms of bandwidth, but they remain the most economical option for storing data at scale. Currently, they account for approximately 80% of all data storage and are predominantly sold into data centers. As AI workloads consume and generate vast amounts of data, these drives are essential for keeping that volume affordable and persistent. This includes checkpoint datasets used to train models and maintain model integrity. It also includes growing volumes of inference-related data, particularly from emerging agentic AI systems, which rely on persistent access to large volumes of historical data to support planning, reasoning and autonomous decision-making.

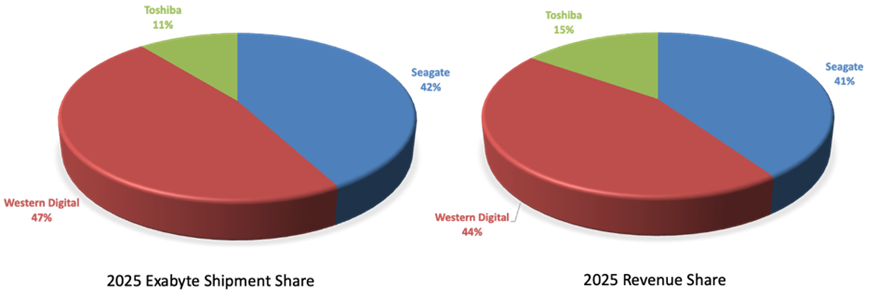

Figure 1: 2025 HDD Market Share

Source: Forbes, Coughlin Associates

This surge in AI-related data volumes is already translating into strong demand for HDDs. The two largest manufacturers (Figure 1), Western Digital (WD) and Seagate, have seen revenues and profits accelerate sharply. For CY26, both companies have already largely sold out their planned capacity, and WD said that three of its top five customers had entered into long-term agreements, with two running through to the end of CY27 and one through to the end of CY28. They are also in conversations regarding CY29 and CY30 capacity. These expanding multi-year customer commitments highlight the growing strategic importance of storage in the AI buildout.

Figure 2: WD Long-term Financial Model (3-5 years)

Source: WD Innovation Date 2026

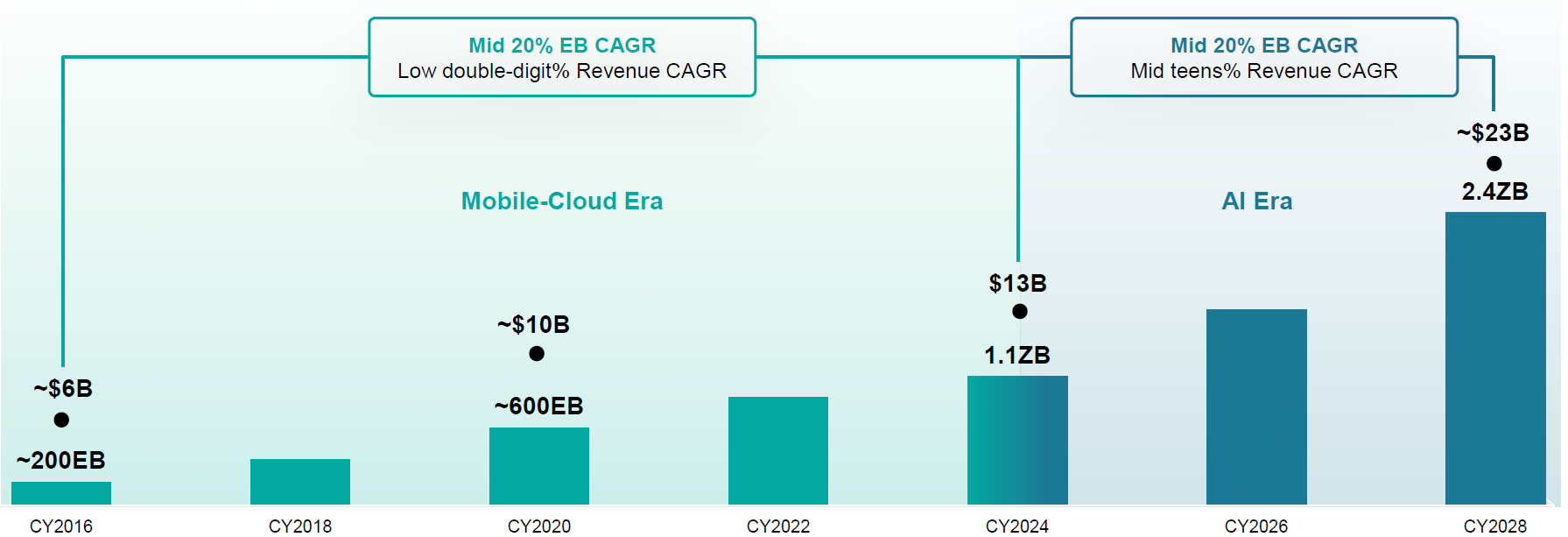

Against this backdrop, HDD manufacturers are guiding for solid growth going forward, with AI-related storage demand catalysing innovation and reshaping their technology roadmaps. During WD’s 2026 Innovation Day, the company guided to an annual revenue CAGR of more than 20% over the next 3-5 years, with data centre HDD capacity shipments (nearline exabytes) guided at a CAGR in the mid-20%s (Figure 2). WD also said pricing is expected to remain stable. IDC has also forecasted a similar exabyte CAGR in the mid-20%s through 2028 for the overall enterprise HDD market (Figure 3).

Figure 3: Worldwide Enterprise HDD Exabyte (EB) Forecast

Source: IDC, Seagate Analyst Day 2025

The growth in capacity is expected to come primarily from increases in capacity per drive rather than from greater unit volumes. For instance, WD recently announced a new 40TB HDD, up from 32TB, as well as a longer-term roadmap to 100TB by 2029. The company is also innovating in areas such as power optimisation and performance, and recently announced new drive technologies that offer 2x bandwidth, with a roadmap to 8x by 2030. These innovations should meaningfully improve HDD performance for AI workloads.

Taken together, HDDs will remain a critical component of AI infrastructure for the foreseeable future, with cost-effective scaling and ongoing innovation continuing to support demand.

It is worth noting that the boundary between HDDs and SSDs is not static. As AI workloads increasingly require higher-speed access, some tiers of storage that were historically served by HDDs may migrate to SSDs over time. However, the sheer volume of data being generated means that HDDs are likely to retain their role as the backbone of bulk storage for the foreseeable future, even as SSDs capture a growing share of higher-performance tiers.

NAND flash and Solid-State Drives

“We are now seeing NAND demand significantly in excess of our available supply for the foreseeable future.”

Sanjay Mehrotra, Micron Chairman, President and CEO (March 2026)

While NAND flash has many use cases, it is currently seeing especially strong demand due to its use in SSDs for AI data centres. SSDs offer several advantages over HDDs, including higher bandwidth, greater density and lower latency, making them well-suited to high-performance workloads. Demand drivers include vector databases and KV cache offloading, with the latter involving moving the KV cache (the working memory used during inference) from scarce and expensive GPU and system RAM onto SSDs. Additionally, shortages of HDD capacity for bulk storage is driving further SSD demand in some parts of the storage stack.

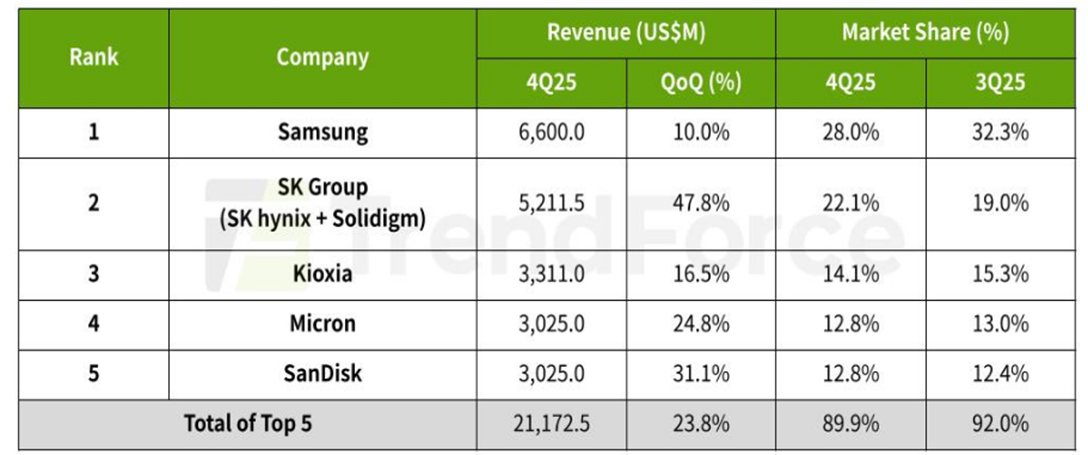

Figure 4: Q4 CY25 Revenue Ranking for Top Five Branded NAND Flash Suppliers

Source: TrendForce

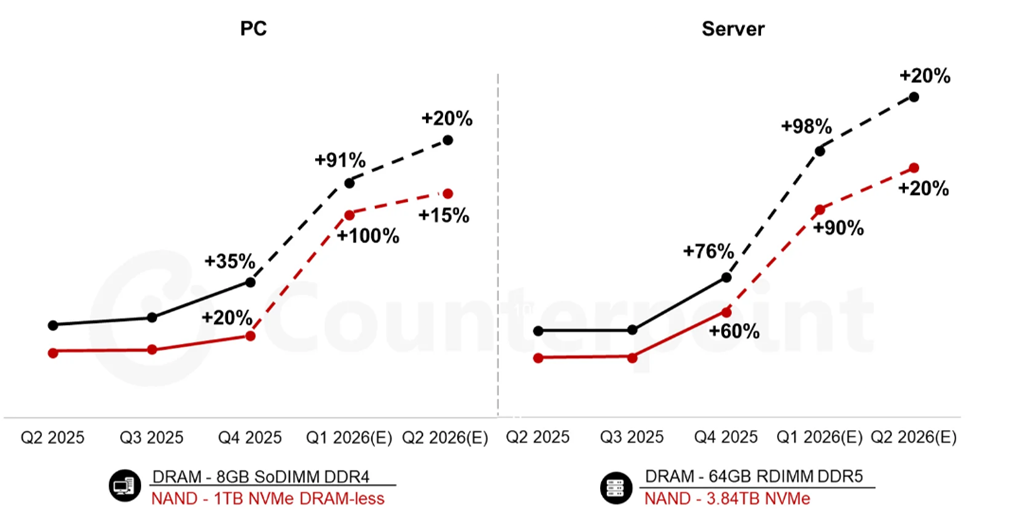

The NAND market is also fairly concentrated, with the top five players accounting for roughly 90% of the market (Figure 4), the balance largely held by China’s domestically focussed YMTC. Overall revenue for these top five suppliers grew 23.8% in Q4 CY25 quarter-over-quarter to cUS$21 billion, driven largely by price increases. This price trend is forecast to accelerate in Q1 CY26, with Counterpoint expecting a 90% surge quarter-over-quarter (Figure 5). This was reflected in Micron’s recent Q2 FY26 results (ended 26 February 2026), where its NAND revenue grew 169% year-over-year and 82% quarter-over-quarter. For CY26, TrendForce forecasts that NAND revenue will grow 112% year-over-year to US$147 billion.

Figure 5: NAND and DRAM Price Trends Q2 2025 - Q2 2026E

Source: Counterpoint

SanDisk Case Study

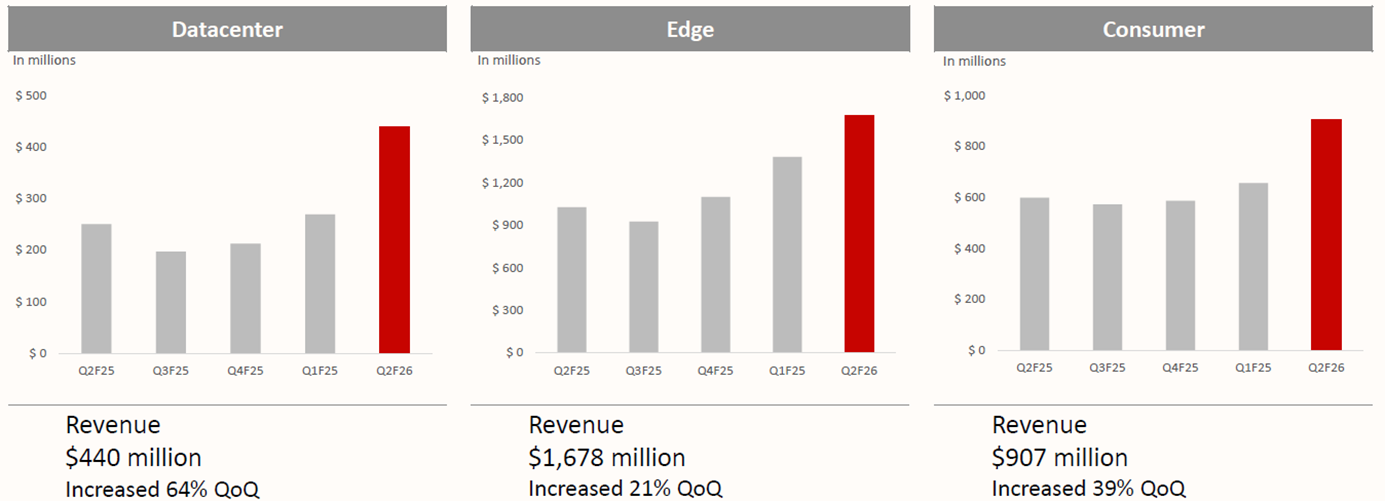

SanDisk is a NAND/SSD pure-play that was spun out of WD in February 2025. As of Q4 CY25, it held a 12.8% market share. The company has benefited significantly from the stronger market backdrop: Q2 FY26 revenue (ended 2 January) rose to US$3 billion, up 61% year-over-year, while GAAP net income margins reached 26.5%. Growth was driven primarily by higher average selling prices rather than volume, with the data centre segment posting the strongest sequential growth at 64% (Figure 6).

Figure 6: SanDisk Revenue Trends by Segment

Source: SanDisk

“There's a whole new category of storage systems and the industry is so excited because this is a pain point for just about everybody who does a lot of token generation today.”

Jensen Huang, Nvidia CEO, CES 2026 (January 2026)

The company has noted that it is in discussions with Nvidia regarding a new KV cache opportunity. At CES 2026, Nvidia unveiled its Inference Context Memory Storage Platform, which adds a dedicated SSD memory layer for KV cache offloading and is set to be available in H2 2026.

Beyond the current demand environment, SanDisk's technology roadmap positions it for the next phase of AI storage. Its new UltraQLC enterprise SSD platform stores four bits per memory cell compared with three in the current standard, delivering higher capacity, lower latency and improved power efficiency. Management noted in January that UltraQLC is now in customer qualification with two hyperscalers, with revenue shipments expected within the next couple of quarters. The company is also developing High Bandwidth Flash (HBF), designed to deliver bandwidth comparable to GPU High Bandwidth Memory but with 8-16x greater capacity at a similar cost, with the first AI inference devices using HBF targeted for early 2027.

“It is our view that this structural evolution is sustainable and should reduce the cyclicality of our NAND business, creating higher average long-term margins and returns.”

Luis Visoso, SanDisk CFO (January 2026)

The more significant question for investors, however, is whether the current demand environment marks a structural break from NAND's past cyclical pattern. Historically, NAND has traded as a commodity through quarterly auctions, leaving suppliers exposed to sharp price swings. But management is now seeing a behavioural shift: similar to the HDD market, SSD buyers are increasingly focused on securing supply rather than negotiating spot prices. SanDisk has signed one long-term agreement, with several more in the queue, and some customers are sharing capacity plans through CY29 and CY30. If the industry can transition towards longer multi-year agreements, it would allow suppliers to plan capacity more effectively while making demand and pricing more predictable – potentially reducing the cyclicality that still weighs on valuations despite the sector's sharp re-rating.

A recent development that is worrying investors is Google Research’s recent TurboQuant breakthrough, announced on 24 March 2026. This is a compression algorithm that the company says can reduce KV-cache memory size by at least 6x and deliver up to 8x performance. On the face of it, this could dampen some of the urgency around NAND demand tied to KV-cache offloading.

However, such efficiency gains cut both ways. If TurboQuant materially improves the return on investment of AI data centres, it could accelerate broader AI deployment and ultimately drive additional infrastructure spending, including on storage. This dynamic (known as Jevons paradox, where efficiency improvements lead to greater overall consumption rather than less) has played out repeatedly across technology cycles. Whether it applies here will depend on the pace and breadth of AI adoption relative to the efficiency gains themselves. This tension between efficiency and demand expansion is arguably the most important variable for the storage thesis more broadly, extending well beyond any single algorithm, and is worth monitoring closely.

Everpure (Pure Storage) Case Study

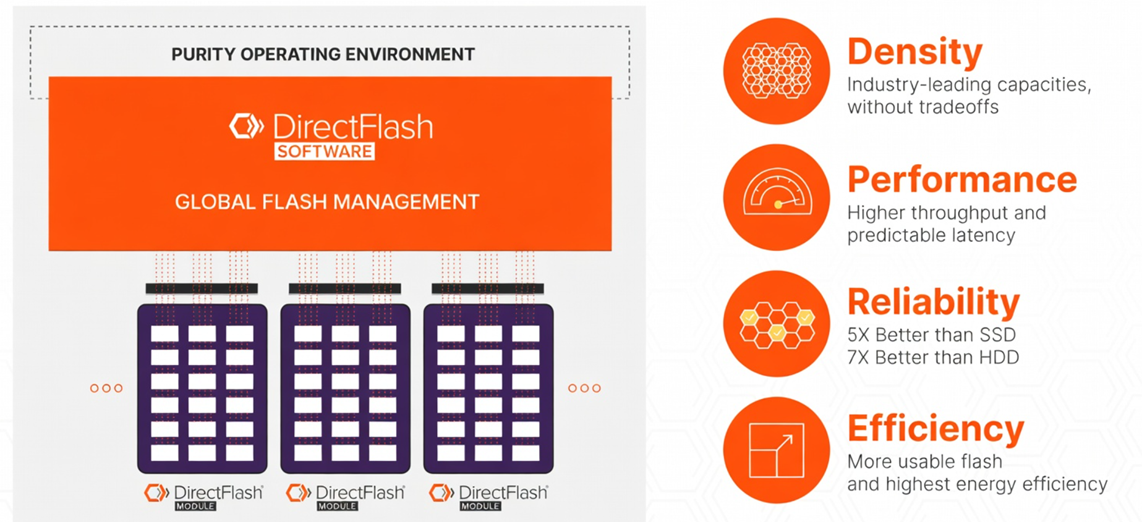

Everpure, formerly Pure Storage, is an enterprise storage platform built on NAND flash. It buys raw NAND and packages it into its own custom DirectFlash Modules rather than relying on off-the-shelf SSDs like many of its competitors (Figure 7). Its software, Purity, is the operating system that communicates directly with the DirectFlash Modules. The benefit of this architecture is that it allows flash management functions such as wear levelling, garbage collection and overprovisioning to be handled at the array level rather than within individual SSDs. Everpure argues that this architecture supports lower power consumption, higher density and greater capacity utilisation of the underlying NAND.

Figure 7: Everpure’s Technology Stack

Source: Everpure

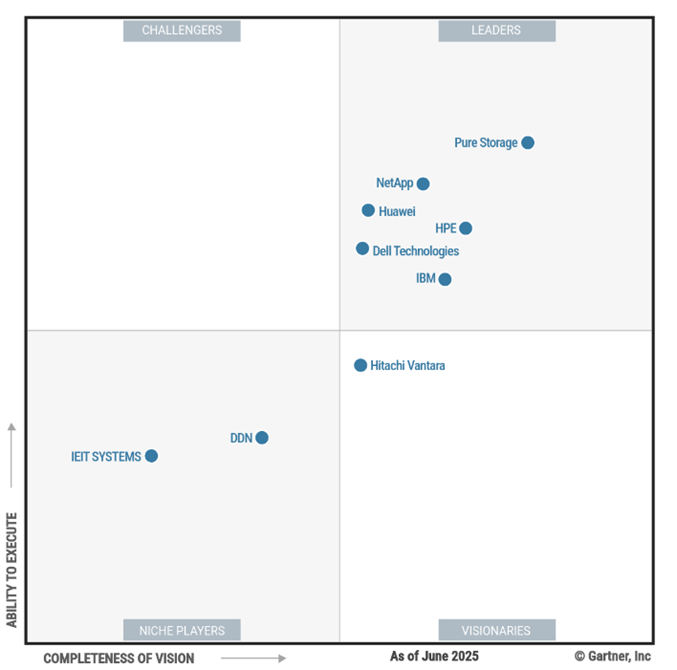

The company is well-regarded in its space, ranking highest on both Ability to Execute and Completeness of Vision in Gartner's Magic Quadrant for Enterprise Storage Platforms (Figure 8), and reporting a Net Promoter Score of 84.

Figure 8: Magic Quadrant for Enterprise Storage Platforms

Source: Gartner

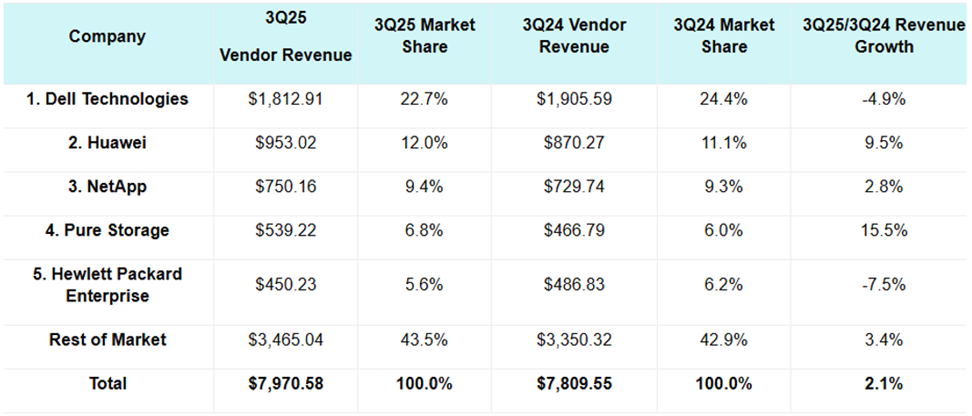

In terms of market share, it ranks 4th in the enterprise storage platform market at 6.8% of the market in Q3 CY25 (Figure 9), though it grew faster than its peers at 15.5% versus 2.1% for the rest of the market.

Figure 9: External Enterprise Storage Systems Market, Q3 CY25

Source: IDC

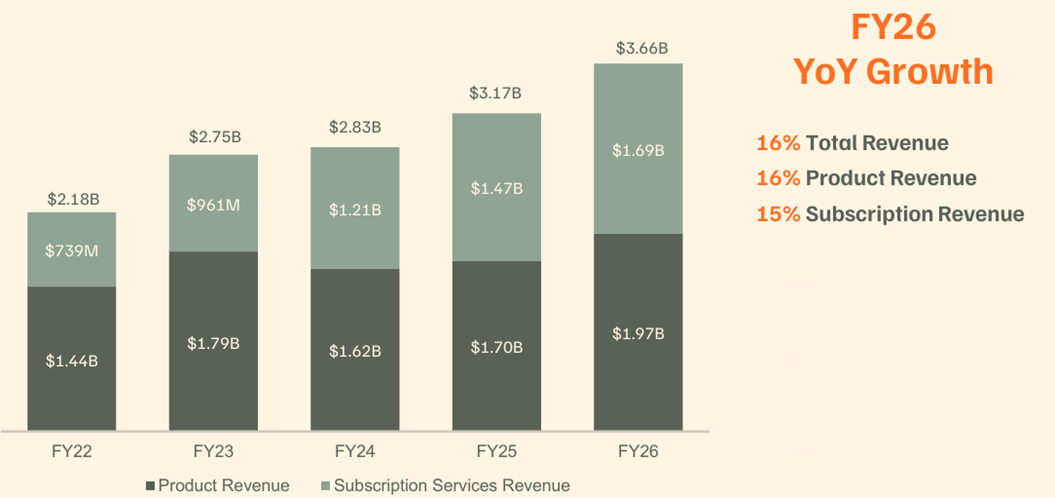

In February 2026, the company rebranded to Everpure to reflect its evolution towards a broader data management platform, and recently agreed to acquire 1touch, a data intelligence and orchestration platform, to strengthen its data discovery and AI-readiness capabilities. In terms of its latest financials, Everpure reported US$3.66 billion in FY26 revenue (ended 1 February 2026), representing 16% growth (Figure 10). It generates revenue from product sales (integrated storage hardware) and subscriptions (Storage-as-a-Service). For FY27, management is guiding for 17%-20% revenue growth, with operating income growing faster at 23%-29%.

Figure 10: Everpure Revenue by Segment

Source: Everpure

The current environment of extreme NAND demand creates both risks and opportunities. For instance, management has warned of supply constraints, though it noted that it has a highly distributed and resilient supply chain to help mitigate these risks. On the positive side, hyperscalers are very eager for capacity. Everpure has seen a footprint expansion with its current hyperscaler customer, Meta, beyond its expectations, and is in engineering test environments with multiple other hyperscalers. Everpure has also recently standardised its hyperscaler business model, under which it will procure some of the components needed by hyperscalers to build the solution in their own environment, while the hyperscalers themselves will procure the NAND through their own supply chains. We expect this will reduce some of the pressure on Everpure’s own supply chain, as hyperscalers are likely better positioned to procure NAND given their greater purchasing scale. Management mentioned that this new business model would be accretive to gross margins.

Overall, amid NAND supply constraints and elevated prices, the ability to maximise usable capacity from each unit of NAND becomes increasingly valuable, potentially putting Everpure in a favourable position in the current environment.

Conclusion

“With some new applications that are coming, we believe the data will become more valuable over time, and that data is going to grow like crazy.”

Dr. Dave Mosley, Seagate CEO (May 2025)

Storage manufacturers have benefited significantly from the ongoing AI data centre buildout, as AI workloads both consume and generate vast volumes of data. We expect this tailwind to continue, particularly as emerging use cases such as AI agents, AI video generation, autonomous vehicles and robotics drive additional demand. This view is reinforced by sustained growth in hyperscaler CapEx budgets, signalling that AI infrastructure investment remains robust.

At the same time, supply growth appears relatively measured; HDD capacity is forecast to grow at around the mid-20%s, while NAND supply is constrained by the multi-year lead times required to bring new fab capacity online. The supply picture is further complicated by YMTC's trajectory and the potential for shifts in trade policy. On the demand side, efficiency breakthroughs such as TurboQuant could either dampen or amplify storage demand depending on whether Jevon's paradox applies. These supply and demand crosscurrents make the outlook more nuanced than a simple extrapolation of current trends

For the long-term structural thesis to hold, several conditions would need to be met, and not all are within the industry's control. AI would need to prove a durable source of demand that delivers clear ROI, sustaining infrastructure investment beyond the current cycle. The shift towards multi-year supply agreements would need to deepen beyond early signings and letters of intent into firm, binding commitments that genuinely lock in volumes and pricing. Capital discipline across the industry, from both established players and emerging Chinese entrants, would need to hold, without a wave of new capacity overwhelming demand. And the current assumption that AI inference workloads will remain heavily concentrated in data centres would need to broadly hold; a faster-than-expected shift towards on-device inference at the edge and endpoint level could meaningfully reduce the volume of data flowing through centralised storage infrastructure. Some of these conditions are observable today, while others such as the trajectory of AI ROI and the long-term architecture of inference will only become clear over a period of years, which is why the market continues to price meaningful cyclical risk into the sector despite the strong near-term fundamentals.

The signposts to watch are: the pace and breadth of long-term agreement signings, the trajectory of hyperscaler CapEx, the commercial impact of efficiency breakthroughs on overall AI deployment, and any shifts in the competitive supply landscape. If these conditions hold, valuations that still embed significant cyclical risk could have further room to re-rate. If they do not, the sector's history suggests that the correction can be sharp.

At AlphaTarget, we invest our capital in some of the most promising disruptive businesses at the forefront of secular trends; and utilise stage analysis and other technical tools to continuously monitor our holdings and manage our investment portfolio. AlphaTarget produces cutting edge research and our subscribers gain exclusive access to information such as the holdings in our investment portfolio, our in-depth fundamental and technical analysis of each company, our portfolio management moves and details of our proprietary systematic trend following hedging strategy to reduce portfolio drawdowns. To learn more about our research service, please visit https://alphatarget.com/subscriptions/.