Introduction

“The interconnection grid is not going to survive all of this new power. There’s not enough switches, there’s not enough wires, there’s not enough management.”

Eric Schmidt, Former Google CEO, May 2026 (SCSP)

Energy remains one of the largest constraints on the AI data centre buildout. The problem is not a shortage of electricity in aggregate, but a shortage of deliverable power in the right locations. The ageing grid was not designed for this scale of load growth, with large AI campuses now requiring several gigawatts (GW) of power. While grid upgrades are underway, they typically have longer timelines than data centre construction. This mismatch has already caused significant project delays and an estimated 30-50% of data centre capacity scheduled to come online in 2026 is now expected to slip.

However, as is often the case, capitalism finds a way. Data centre developers are increasingly turning to behind-the-meter power, where electricity is generated on or near the site and used directly by the facility. Onsite gas turbines have been one of the more prominent solutions, but this market is now also facing long lead times and permitting challenges as local communities push back against the air pollution caused by these systems. Developers are increasingly pivoting to fuel cells, offering faster deployment and materially lower emissions than combustion-based alternatives. The most visible beneficiary has been Bloom Energy, which has seen extraordinary sales growth in recent quarters and a share price that has risen more than 1,400% over the past year (as of this writing), raising the question of how much of the opportunity is already priced in.

In this note, we first provide an overview of the grid constraints holding back AI data centre deployment. We then examine the growing use of behind-the-meter power, looking first at onsite gas turbines before outlining why fuel cells are emerging as a credible alternative. Next, we provide a case study on Bloom Energy, including the drivers of its recent momentum and the risks facing its growth thesis. Finally, we explore lesser-known fuel cell players such as Ceres Power and its manufacturing partners before setting out forecasts for the scale of the opportunity.

The Problem: the Grid

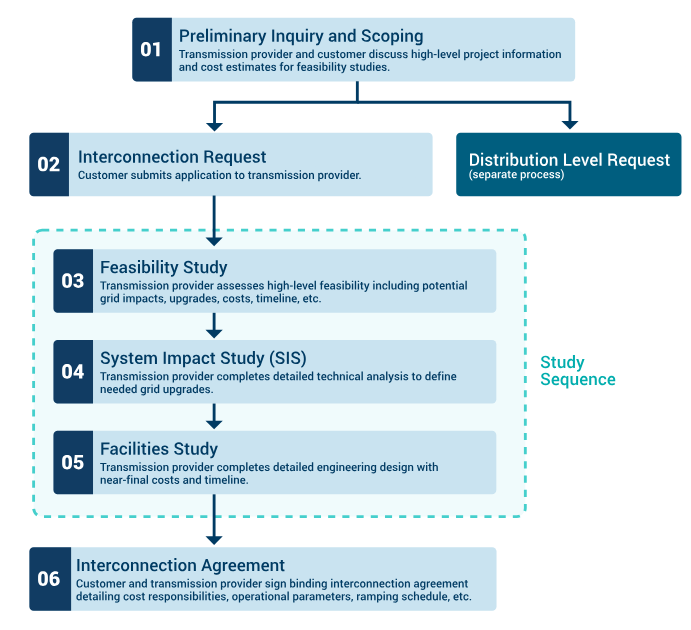

The process of connecting to the grid can be lengthy and complex. When a data centre requests capacity, grid operators need to evaluate whether the existing transmission lines, substations and related infrastructure can accommodate the additional demand and whether upgrades or new infrastructure are necessary (Figure 1). Given the vast amount of power these sites require, new infrastructure is often required. Planning, permitting and completing significant new grid infrastructure can often take between 5 to 15 years, whereas data centre builds typically take 1 to 3 years, according to the International Energy Agency. This creates a significant timing mismatch.

Figure 1: Connecting to the Grid Steps

Source: Rocky Mountain Institute (RMI)

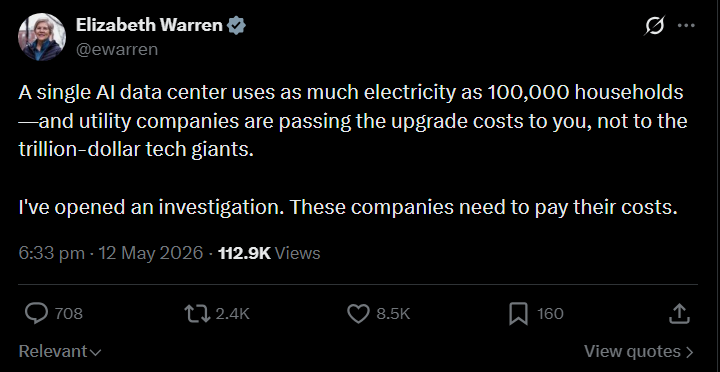

In addition to the lengthy timelines for connecting to the grid, there is also often local opposition over concerns that large data centre grid connections will increase electricity costs for consumers. In March 2026, Amazon, Google, Meta, Microsoft, OpenAI, Oracle and xAI signed the Ratepayer Protection Pledge issued by the White House, “agreeing to build, bring or buy new generation resources and cover the cost of all power delivery infrastructure upgrades required for their data centers, ensuring such expenses are not passed to American households.” However, public opposition and political scrutiny remain, with Senator Elizabeth Warren opening an investigation in May 2026 in which she claimed tech giants were not paying their fair share (Figure 2).

Figure 2: Senator Elizabeth Warren Opens Investigation Into Tech Giants

Source: X

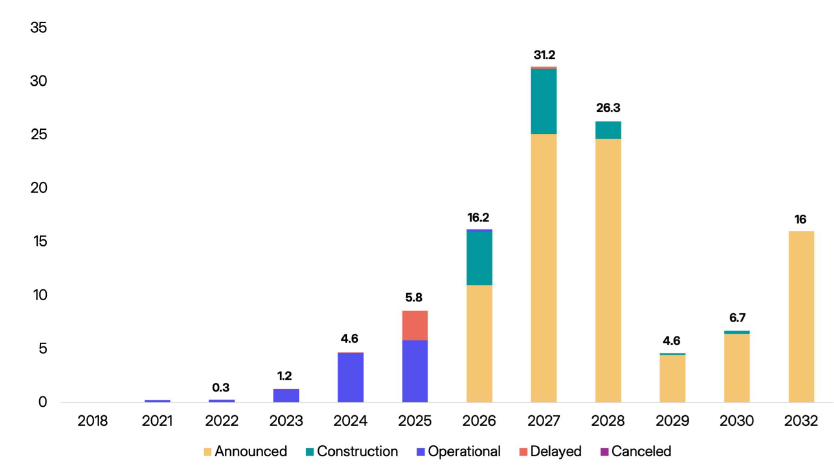

As a result of both grid constraints and public opposition, 30–50% of data centre capacity scheduled to come online in 2026 is expected to be delayed, according to Sightline Climate. This follows a difficult 2025, when 26% of expected capacity slipped and another 10% of projects pushed back their commercial operation dates without much notice (Figure 3).

Figure 3: Data Centre Pipeline, by Operational Date (GW)

Source: Sightline Climate

The Solution: Behind-the-Meter Power

“Time to power is incredibly important, that’s what really everyone cares about.”

Thomas Schuldt, VP Business Development & Strategy, DG Matrix, February 2026 (Sightline Climate)

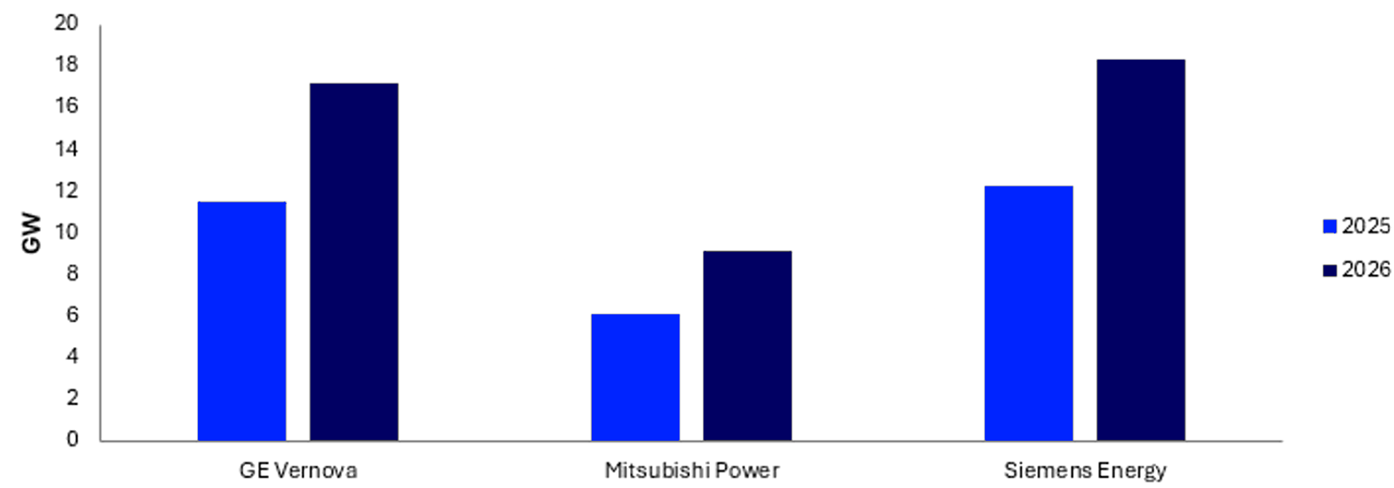

Given the challenges of securing power from the grid, data-centre developers are increasingly turning to behind-the-meter solutions. This refers to electricity generated on or near the data-centre site and used directly by the facility rather than being supplied through the public grid. The idea is not new, but AI has pushed it from a niche workaround towards a mainstream development strategy, with xAI’s 2024 use of onsite gas turbines to power its Memphis data centre bringing the model into the spotlight. The most obvious behind-the-meter option has been gas turbines, but due to strong demand, that market has also become constrained. GE Vernova, Mitsubishi Power and Siemens Energy make up the majority of this market and are seeing significantly more demand than they can supply, with lead times now at around 3–4 years. Additionally, gas turbine prices have risen sharply, with Wood Mackenzie estimating that between 2019 and the end of 2027 prices will have risen 195%.

Figure 4: Gas Turbine Manufacturing Capacity

Source: Wood Mackenzie

Behind-the-meter solutions are also facing backlash due to concerns about their impact on local communities. In April 2026, xAI was sued by NAACP and its Mississippi State Conference over unpermitted turbines in Mississippi, where there were concerns that the air pollution they emitted, such as smog-forming nitrogen oxides (NOx) and carbon monoxide, could impact the health and wellbeing of surrounding neighbourhoods. The plaintiffs are asking the court to force xAI to stop operating unpermitted turbines, install best available control technology and assess financial penalties. xAI had already removed some of its turbines earlier in response to a prior notice of intent to sue. Similarly, Oracle’s Project Jupiter in New Mexico, has also faced local opposition and legal challenges against county approvals for the project. Oracle and BorderPlex have since announced that the project’s previously planned gas turbines and diesel generators will be replaced by up to 2.45 GW of fuel cells from Bloom Energy.

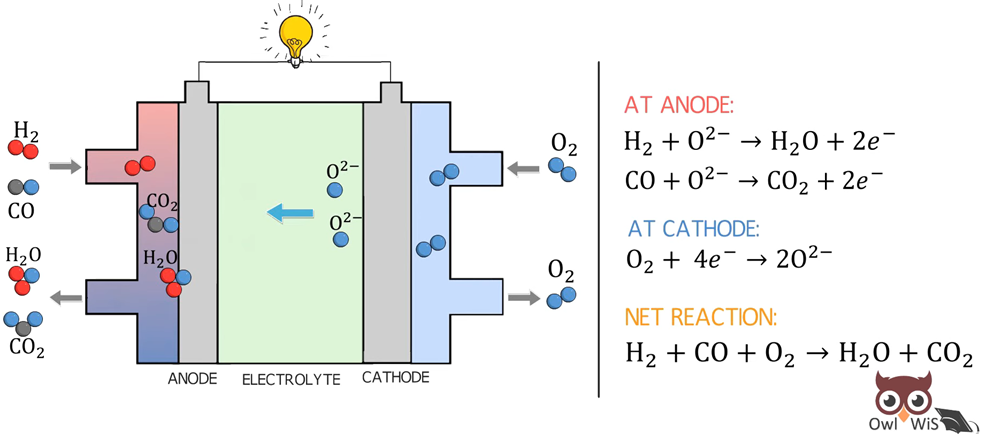

Oracle is not an isolated example of data-centre developers turning to fuel cells. This form of behind-the-meter power is increasingly being adopted because it offers several advantages over gas turbines, including materially lower air pollution, quieter operation and lower water requirements, making fuel cells more acceptable to local communities. In simple terms, a fuel cell is an electrochemical device that converts chemical energy in a fuel into electricity and heat without conventional combustion. At its core, a fuel cell consists of two electrodes, an anode and a cathode, as well as an electrolyte. Fuel is supplied to the anode and air or oxygen is supplied to the cathode; the electrolyte allows ions to move between the two electrodes while electrons flow through an external circuit, creating usable electricity. Different fuel-cell technologies use different electrolytes, such as solid oxide or molten carbonate. Different systems can run on different fuels based on design. For data centres, solid oxide fuel cells are currently the most relevant fuel-cell technology, owing to their high electrical efficiency and fuel flexibility (e.g., typically fuelled by natural gas, but can also run on hydrogen or biogas).

Figure 5: Solid Oxide Fuel Cell

Source: Owl WiS

Leading the Charge: Bloom Energy

“We will strive to bring power to our customers faster than they can stand up their greenfield facilities. We were able to make that promise because we invested deliberately ahead of demand.”

KR Sridhar, Bloom Energy CEO, Q1 2026

Bloom Energy was founded in 2001 by KR Sridhar, drawing on his earlier NASA-related work in solid oxide electrochemistry at the University of Arizona. While developing a method to produce oxygen and fuel for use on Mars, Sridhar’s team realised that the same technology could be used in reverse to generate electricity from oxygen and fuel on Earth. In 2008, Bloom launched the Bloom Energy Server commercially, its proprietary high-temperature solid oxide fuel cell system for distributed power generation. Nearly two decades later, after years as a relatively niche onsite power solution, Bloom’s Energy Server is seeing a sharp acceleration in demand as the AI data centre buildout increases power needs and legacy power solutions struggle to keep up.

Bloom’s Financials

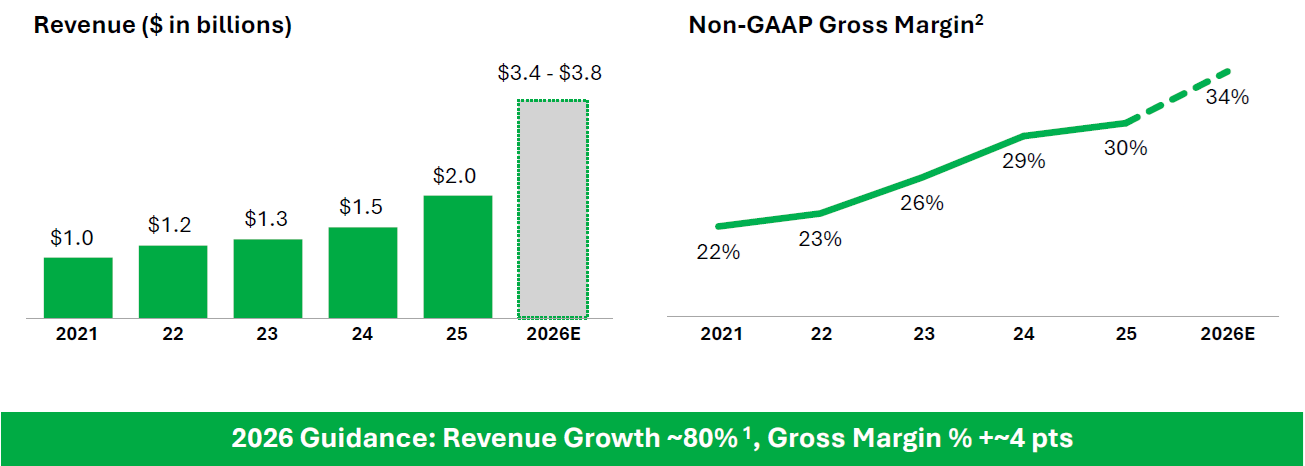

In Q1 2026, its product revenue grew 208% year-on-year to US$653.3 million, accounting for 87% of the company’s revenue. Overall revenue for Q1 was up 130% to US$751.1 million. Bloom’s smaller segments include revenue streams from installation, electricity sales and services. Service revenue accounts for just under 9% of total revenue and comes from operations and maintenance agreements, which have a 100% attach rate to the product and an average duration of 10–15 years. For FY 2026, the company is guiding to 80% revenue growth (Figure 6).

Figure 6: Bloom Energy’s Financial Performance and FY26 Forecast

Source: Bloom Energy

Bloom’s Advantage

In addition to the community-related advantages of fuel cells discussed previously, Bloom’s systems offer several other benefits that have also driven demand. According to management, the key advantage is time to power, where Bloom’s Energy Servers can be available in as little as 90 days; for instance, the company highlighted an Oracle deployment that was completed in just 55 days, more than a month ahead of schedule. Bloom is also currently neither order nor capacity constrained, with a manufacturing footprint that can support 5 GW of annual product output. Bloom’s management has also said they will never be the bottleneck for customers and can build additional capacity faster than any other option in the market. Additionally, its systems are modular, which means they can easily scale with the project’s power needs (Figure 7). Furthermore, at 99.999% uptime, Bloom claims its systems have higher reliability than the grid and that the power output can be adjusted within seconds. Lastly, its energy servers have an internal operating temperature of around 800°C, generating high-grade exhaust heat that can be captured and converted into chilled water through absorption chillers, which is ideal for data centre cooling.

Figure 7: Fuel Cell to Energy Server Farm

Source: Bloom Energy

Bloom’s Economics

“We are already at parity with other technologies, but very soon we will also be the cheapest as we scale up.”

Aman Joshi, Bloom Energy Chief Commercial Officer, March 2026 (EnergyCents Podcast)

In terms of cost, Bloom says its systems are currently competitive with other technologies. In the EnergyCents podcast, Bloom’s Chief Commercial Officer, Aman Joshi, broke down how its cost structure compared to gas turbines. There he said Bloom’s systems currently cost US$5,000/kW, but they qualify for tax credits, reducing the cost by 30-40%, bringing the net cost down to US$3,000/kW at 40% tax credits. This is still more expensive than gas turbines at roughly US$2,500/kW. However, Bloom has an average fuel efficiency of 54–55% over a 20 year period, which Joshi compared to gas turbines that start at around 40% and degrade significantly over time. Gas turbines also have far lower efficiency at partial loads, compared to more stable efficiency of Bloom’s solution. This efficiency benefit provides significant savings over the life of the system. Joshi also mentioned that, unlike gas turbines, Bloom’s technology does not need batteries. Additionally, fuel cells produce DC power, while gas turbines and grid connections deliver AC power. This is an important advantage as Nvidia transitions from traditional 415/480VAC data centre power architectures towards 800VDC for future high-density AI racks. With Bloom’s Energy Server being 800VDC-ready, the platform aligns with future DC rack architectures and avoids costs related to the front-end AC/DC conversion stage required by AC-based power sources.

“We remain the only on-site generation solution with a sustained downward sloping cost curve.”

KR Sridhar, Bloom Energy CEO, Q1 2026

Bloom has also been reducing product costs by around 10% annually and expects this to continue as it benefits from scale, technology innovation and manufacturing improvements. This puts the company on a path to become a lower-cost alternative to competing onsite power sources while supporting margin expansion. Combined with easier permitting and shorter time to power, which also significantly improve project economics, Bloom should remain a highly competitive solution going forward.

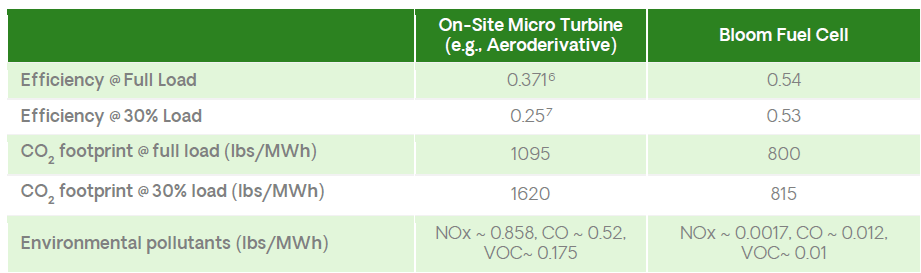

Figure 8: Bloom Fuel Cell vs On-Site Micro Turbine (February 2024 Data)

Source: Bloom Energy

Bloom’s Risks and Constraints

There are however some risks and constraints around Bloom’s future growth. Most deployments rely on natural gas, meaning Bloom’s systems still produce emissions (Figure 8). Even though these are materially lower than combustion-based alternatives, this can still create permitting and reputational risk, particularly for hyperscalers with clean-energy commitments or projects facing local scrutiny. In 2024, DCD reported that Amazon withdrew plans to use Bloom natural-gas fuel cells at Oregon data centres after criticism that the project would increase the sites’ carbon footprint. In February 2026, DCD also reported that the City of Hilliard in Ohio challenged a proposed 73 MW Amazon fuel cell project over air-quality and local-review concerns.

There is also a longer-term demand risk if customers use fuel cells only as a temporary speed-to-power solution rather than as permanent primary power. In Hilliard, Amazon said the fuel cells would temporarily power part of its data-centre operations while broader power infrastructure upgrades in Ohio were completed. However, we do not view this as a major risk as grid upgrades are likely to remain too slow and uncertain across many markets, meaning fuel cells will often remain the best available option. Finally, natural gas fuel cells also require a constant gas supply that meets its fuel specifications, making gas access a real site-selection constraint.

The Underdogs: Ceres Power and Co.

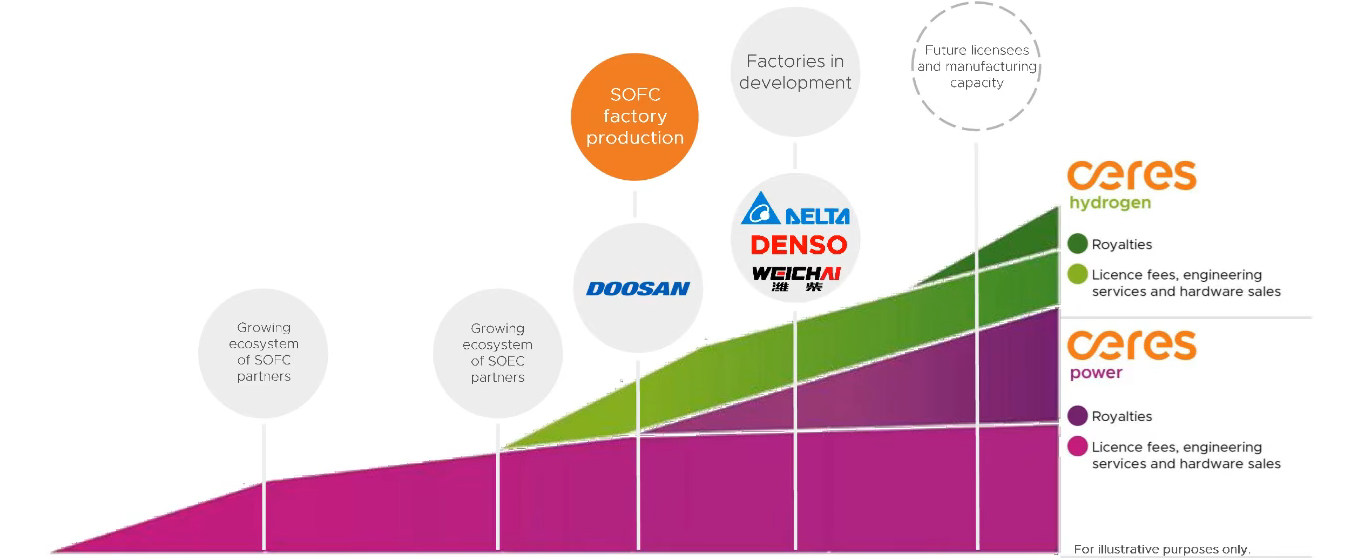

Although Bloom Energy has received most of the attention in the fuel cell space, it is not alone in pursuing solid oxide technology. Ceres Power is a smaller UK-based rival that generated £32.6million of revenue in 2025. Like Bloom, it was founded in 2001, having been spun out of Imperial College to commercialise its solid oxide technology. However, Ceres has taken a different commercial path. Rather than manufacturing end products itself, it licenses its cell and stack technology to partners, similar to Arm’s IP model for CPUs (Figure 9). Though unlike Arm’s ubiquity, Ceres’ royalty stream depends on a small number of partners successfully scaling production and winning end-customers. Manufacturing partners for its solid oxide fuel cells include Doosan Fuel Cell and Delta, with Doosan becoming the first to enter mass production in mid-2025. Ceres also has a hydrogen business, developing solid oxide electrolyser technology for green hydrogen production with partners such as Shell. In addition to licence revenue, Ceres earns royalties when partners sell products using its technology, which is where it expects to generate the bulk of its revenue over time, at a rate of US$50-100 million per GW of partner production. This is likely at a very high margin, though a fraction of the approximate US$5 billion in revenue per GW that Bloom achieves for selling the full system it produces.

Figure 9: Ceres revenue streams from license and royalties

Source: Ceres

In April 2026, Ceres launched its Endura technology platform, which is designed to serve both its power and hydrogen markets through a single architecture. Although it is difficult to assess how the overall technology compares with Bloom’s, one key distinction is operating temperature. Ceres’ technology operates at 450–630°C compared with Bloom’s technology which operates above 800°C. Operating at a lower temperature allows Ceres to use more widely available, cost-effective and recyclable materials, reducing overall fuel cell system costs by around one-third and lowering supply-chain risk. Ceres also claims 65% efficiency using natural gas, with performance maintained through the product life, making it more efficient than Bloom. If its overall technology proves to be competitive with Bloom’s, Ceres and its partners could become credible rivals, with management’s view that the market is large enough for both.

However, there are other fuel cell companies targeting the data center market. This includes FuelCell Energy, which uses molten carbonate fuel cells; PowerCell, which uses hydrogen-based PEM fuel cells; and GE Vernova, which is also developing its own solid oxide fuel-cell technology. We expect the competition to intensify given the size of the AI data centre opportunity.

Sizing the Opportunity

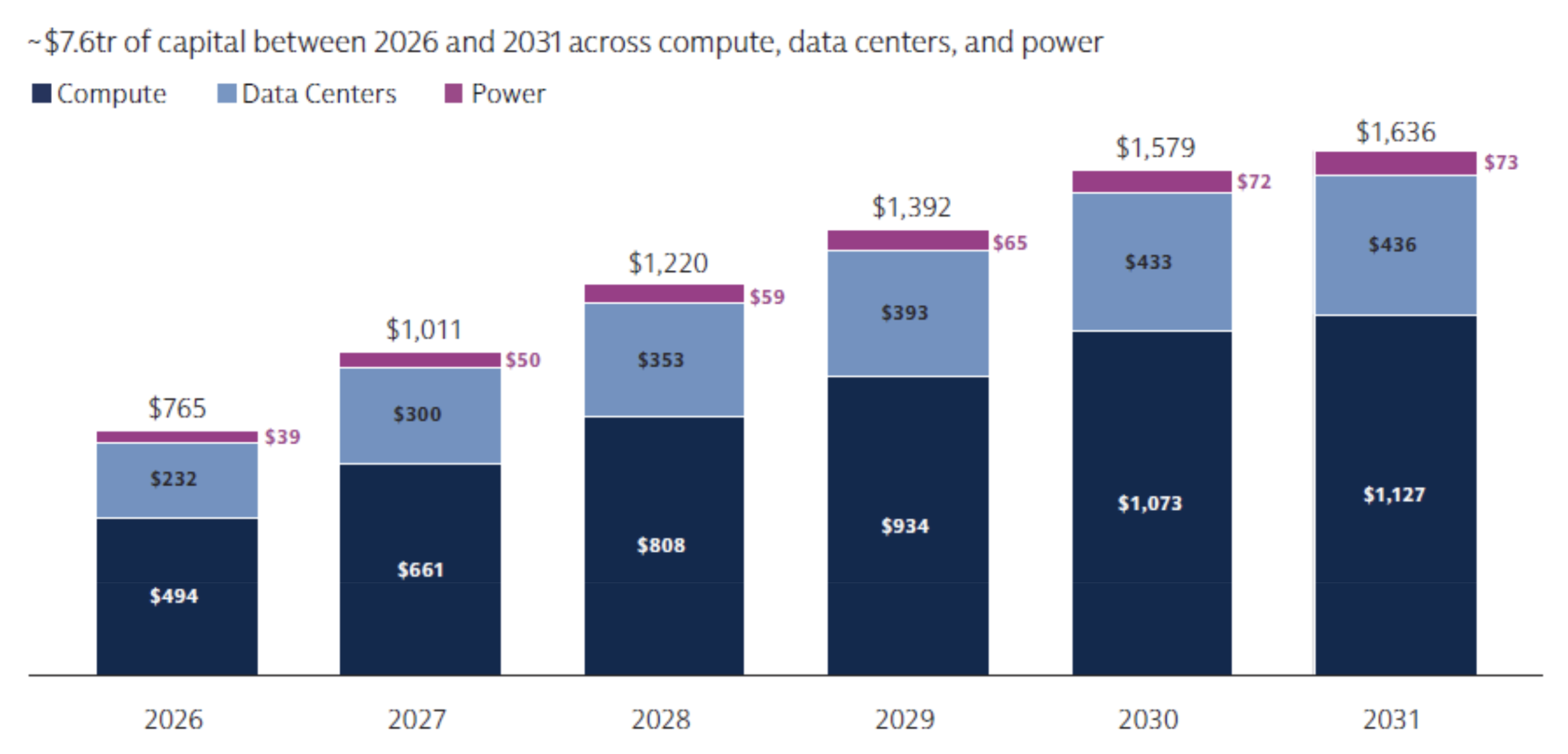

Goldman Sachs’ baseline scenario estimates around US$7.6 trillion of AI infrastructure CapEx between 2026 and 2031, spanning compute, data centres and power (Figure 10). Annual spending rises from US$765 billion in 2026 to around US$1,636 billion in 2031, though Goldman stresses that these estimates are highly sensitive to assumptions, including the useful life of AI silicon, next-generation data centre costs, chip architecture mix and bottlenecks in power, labour and critical equipment. Within the 2031 estimate, power accounts for only US$73 billion or roughly 4-5% of the total, compared with US$1,127 billion for compute and US$436 billion for data centres. While power represents only a small share of total CapEx, its role as a gating factor means availability and speed of deployment generally matter more than the absolute cost of the power equipment itself.

Figure 10: AI Capex Estimates (billion)

Source: Goldman Sachs

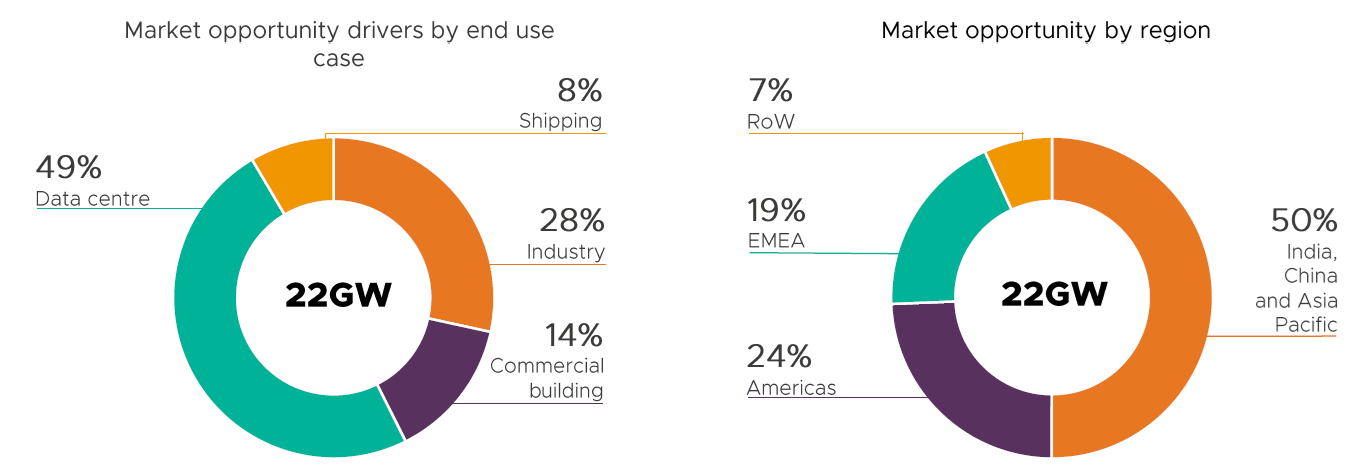

For the solid oxide fuel cell market, Ceres Power estimates, based on its own analysis using BNEF data, that the market will reach 22 GW by 2030 (Figure11). Using an assumed price of US$2,500/kW, this equates to a US$55 billion addressable market. Notably, data centres account for just under half of expected demand in this scenario, with the remainder driven by industry, shipping and commercial buildings. Regionally, Ceres expects the Americas to represent only 24% of the market, while India, China and Asia Pacific account for 50%.

Figure 11: Global market opportunity for solid oxide fuel cells by 2030

Source: Ceres Power, BNEF New Energy Outlook Data 2025

Conclusion

Behind-the-meter power is becoming one of the clearest solutions to the current grid bottleneck, with fuel cells increasingly standing out as one of the most compelling options. They combine fast deployment, materially lower emissions than combustion-based alternatives and alignment with emerging 800VDC data centre architectures. That makes them exceptionally well placed for AI data centres, where power availability is now a gating factor rather than a secondary consideration. Among fuel cell players, Bloom Energy has been the clearest beneficiary so far, though other players in the space such as Ceres Power could still become credible competitors if they prove their technologies at scale.

However, fuel cells are not the only emerging solution. The market is becoming increasingly creative as developers look for credible ways to bring power online faster. One example is Boom Supersonic, which is repurposing jet-engine technology into natural-gas turbines for AI data centres. Batteries are also likely to become more important for grid support, backup and smoothing demand spikes. Over the longer term, nuclear, fusion and orbital data centres could also become part of the answer. Even so, fuel cells have several differentiated characteristics and are on a trajectory to become more competitive over time, leaving them well placed to become a significant part of the data centre power solution going forward.

At AlphaTarget, we invest our capital in some of the most promising disruptive businesses at the forefront of secular trends; and utilise stage analysis and other technical tools to continuously monitor our holdings and manage our investment portfolio. AlphaTarget produces cutting edge research and our subscribers gain exclusive access to information such as the holdings in our investment portfolio, our in-depth fundamental and technical analysis of each company, our portfolio management moves and details of our proprietary systematic trend following hedging strategy to reduce portfolio drawdowns. To learn more about our research service, please visit https://alphatarget.com/subscriptions/.