The financial technology (fintech) and digital payments industries encompass a broad range of financial services that leverage technology to enhance or automate financial processes and services.

Fintech refers specifically to the integration of technology into offerings by financial services companies to improve their use and delivery to customers. Early stage fintech companies are typically founded with the intent of disrupting incumbent financial institutions and corporations that rely less on software and technology as cornerstones of their respective businesses.

Some of the primary products and services offered by fintech businesses include:

- Digital payment solutions: Facilitating the exchange of money between parties through various digital methods, rather than cash or cheques.

- Personal finance and wealth management: Providing digital banking solutions, financial management and financial planning services directly to consumers.

- Lending services: Including peer-to-peer or marketplace lending platforms, which connect borrowers directly to lenders through digital platforms.

- Insurance technology (Insurtech) platforms: Using technology to simplify and streamline the insurance industry, handling everything from underwriting to claims processing and fraud detection.

- Cryptocurrencies and Blockchain products: Implementing new financial technologies for creating, managing, and transacting cryptocurrencies, and using blockchain technology for secure transactions and record-keeping.

The fintech and digital payments industries are crucial in our modern digital economy, driving innovation in financial transactions and offering consumers and businesses more flexible, efficient, and secure options for managing their financial operations. These industries are nascent and continually evolving, propelled by technological advancements and growing digital connectivity.

Current state of the industry

The fintech industry has continued to experience remarkable growth and transformation in recent years, solidifying its position as a crucial player in the global financial landscape. As of now, the industry is thriving, driven by a combination of technological advancements, evolving consumer preferences, and regulatory changes.

Fintech companies are revolutionising traditional financial services by leveraging artificial intelligence, machine learning, blockchain, and cloud computing to deliver innovative and user-friendly solutions. The adoption of mobile banking, digital payments, and online lending has accelerated, with consumers embracing the convenience, speed, and accessibility offered by these digital platforms. Moreover, fintech has extended its reach beyond retail banking, and expanded into areas such as insurance, wealth management, and capital markets.

In 2023, the banking industry generated more than US$7 trillion in revenues with year-over-year growth in volume and revenue margins. Fintech accounted for just 5 percent of the global banking sector’s net revenue! This shows that the penetration rate is still very low and the industry should continue to grow for several years. McKinsey & Company estimates that the fintech industry’s revenue is likely to double to more than $400 billion by 2028, representing a 15 percent compound annual growth rate vs. the overall banking industry’s compound growth rate of roughly 6 percent.

The digital payments market has also experienced significant growth and transformation over the past 20-plus years, led by a combination of technological innovation, increasing global digitalisation and changing consumer preferences.

According to Statista (Figure 1), the transaction value of digital payments completed annually has more than tripled since 2017 and it is expected to reach US$11.53 trillion in 2024.

Figure 1: Steady growth in digital payments

Source: Statista

E-commerce transactions have historically represented an outsized share of the world’s total digital transaction value, and will likely continue to do so for the foreseeable future. As we noted in our recent e-commerce industry report, e-commerce currently accounts for a surprisingly low 20% of total retail sales worldwide and this figure is expected to expand to 23% of total retail sales by 2027.

The penetration rates are even lower in most of the developing nations where e-commerce represents just 7-9% of total retail sales. In our view, this is a major growth opportunity and the increasing adoption of e-commerce should serve as a meaningful tailwind for digital payments.

Fintech is a good industry

Fintech and online payments have some attractive business characteristics which is why we have invested a portion of our capital in a few promising companies in this industry. Here are some of the favourable attributes of fintech businesses -

High growth potential: The fintech and payments industry is characterised by rapid growth, driven by the increasing adoption of digital solutions across banking, investments, and everyday transactions. As more consumers and businesses embrace digital and mobile payment solutions, companies operating in this space continue to expand their market reach and service offerings, offering significant growth opportunities for investors.

Low cost structures: Digital companies’ overheads tend to be far lower than traditional banks. For example, fintech players do not need to invest in extensive networks of physical branches so they do not have to employ as many employees as the legacy financial institutions. This significantly reduces their operating expenses and capital requirements; and improves margins. Moreover, fintech businesses lean more on cutting-edge technology/software solutions to handle almost every aspect of their businesses, and this further enhances their offerings whilst cutting down on their human resources costs.

Passing on cost savings: Often, fintech companies pass along the resulting cost savings of their digital foundations to their customers and this enables them to grab market share. For instance, digital banks and online lenders typically offer more favourable interest rates on savings or loans; meanwhile “Insurtech” companies are able to underwrite policies with lower premiums and superior combined ratios. Since fintech companies have lower cost structures, they are able to invest more in technology which results in customer benefits such as top-notch fraud detection, faster claims processing and quicker loan approvals. These enhanced services attract more customers and enable these businesses to grow.

Frequent, repeat purchases: Fintech is known for its stickiness as customers stay loyal and engage in frequent repeat transactions. Payments and banking are inherently sticky industries i.e. once customers sign up, unless they are very disappointed, they tend to stay. This can be attributed to the innovative and diverse solutions offered by fintech companies, which address specific pain points in the financial industry. The comprehensive service offerings provided by fintech companies enhance customer satisfaction and encourage consolidation of financial activities. Frequent, repeat transactions reduce cyclicality and generate more stable cash flows for these businesses.

Rapid diversification of services: Fintech companies disrupt traditional financial sectors including banking, insurance, and asset management by continuously introducing new products and services. This diversification not only attracts a broader range of consumers and makes the company’s offerings more “sticky”, this spreading of revenue streams across different financial services also mitigates business risk.

Financial inclusion: Fintech companies often provide financial services to underserved or unbanked populations, particularly in emerging economies. For instance, over the past decade, mobile payment systems have enabled transactions and financial management in much of the developing world without the need for traditional bank accounts, thereby opening up the financial system to a larger subset of the population. Globally, 76% of adults have a bank account today, up from 51% a decade ago! This is not only good for society, it is also a solid opportunity, as it allows fintech businesses to tap into previously unreachable customers who are often disenfranchised with their countries’ long-established financial institutions.

As financial technology continues to evolve, the industry's significance is expected to increase further. It is notable that key fintech players such as PayPal, Ant Group, Stripe and Square parent Block have already achieved impressive scale given their early industry leadership. Meanwhile, startups such as digital banking leader SoFi Technologies, Brazilian fintech StoneCo, and U.S.-based insurance company Lemonade have also stormed onto the scene in recent years, bringing innovative solutions to the market, which is good for consumers.

Sizing the opportunity

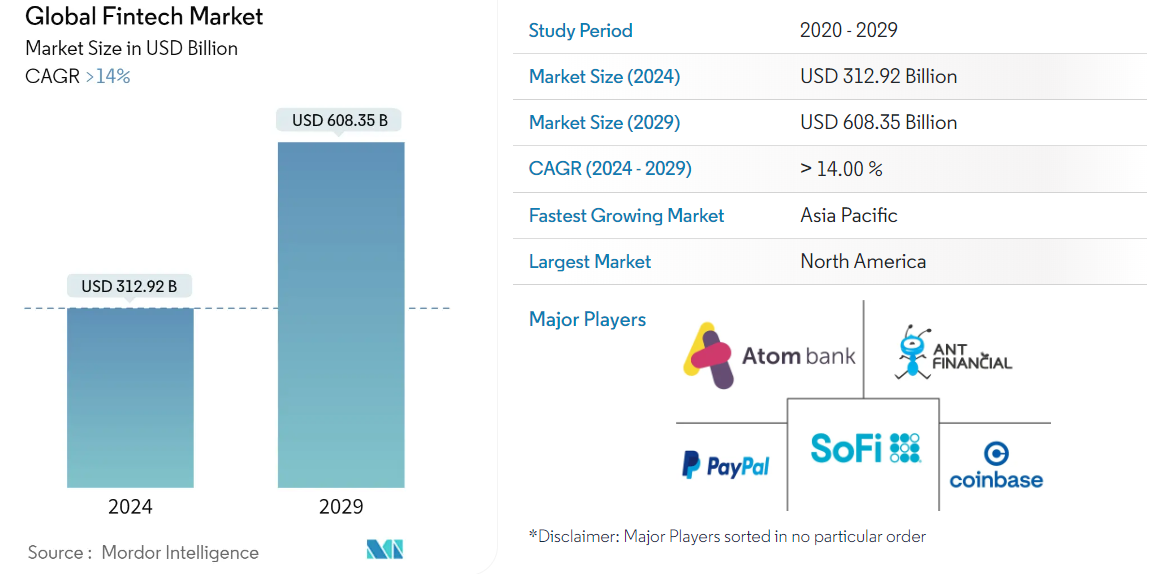

The fintech industry is still fairly young and it is likely to continue its steady growth over the next decade. It is interesting to note that Mordor Intelligence expects the global fintech market to nearly double in value to $608 billion over the next five years (Figure 2), representing a compound annual growth rate of over 14% between now and 2029.

Figure 2: Fintech market size to double in 5 years

Source: Mordor Intelligence

If recent industry trends are any guide, much of the industry growth in the future will be fuelled by the developing economies. In 2023, fintech revenues in Africa, Asia–Pacific (excluding China), Latin America, and the Middle East represented 15 percent of fintech’s global revenues. It is estimated that this number will rise to 29 percent in aggregate by 2028! Conversely, last year North America accounted for 48 percent of worldwide fintech revenues and this number is expected to decrease to 41 percent by 2028.

Today, fintech penetration in the developing world is the highest in the world. This is not surprising given that up until recently, many of these nations lacked access to basic banking services which gave fintech companies the opportunity to serve unmet needs.

Due to the explosive adoption of smartphones over the past 15 years, fintech services have proliferated in the developed world. Despite this progress, the World Bank recently estimated that there are still 1.4 billion unbanked adults worldwide and most of them are in the developing world. According to the World Bank’s Global Findex report, approximately 29% of adults in the developing world still do not have a bank account and this is a major business opportunity for fintech companies in Africa, Asia and South America.

The fintech industry’s explosive growth over the past 5 years has created significant wealth for investors. According to McKinsey & Company, as of July 2023, publicly traded fintech companies represented a market capitalisation of US$550 billion, a two-times increase versus 2019. In addition, as of the same period, there were more than 272 fintech unicorns, with a combined valuation of US$936 billion, a sevenfold increase from 39 firms valued in excess of US$1 billion just 5 years ago!

In our view, the high quality, dominant fintech businesses with good unit economics will continue to prosper over the following years and that will be rewarding for their shareholders.

Just like any industry though, not all businesses are created equal and there will be winners and losers. Therefore, investors will have to carefully evaluate potential businesses before committing their capital.

At AlphaTarget, we invest our capital in some of the most promising disruptive businesses at the forefront of secular trends; and utilise stage analysis and other technical tools to continuously monitor our holdings and manage our investment portfolio. AlphaTarget produces cutting-edge research and those who subscribe to our research service gain exclusive access to information such as the holdings in our investment portfolio, our in-depth fundamental and technical analysis of each company, our portfolio management moves and details of our proprietary systematic trend following hedging strategy to reduce portfolio drawdowns. To learn more about our research service, please visit subscriptions.